MiCA Regulation Crypto Guide: The Complete MFSA Rulebook 2025 Explained

Table of Contents

- What Is MiCA Regulation and Why It Matters

- Scope and Application of the MiCA Rulebook

- CASP Licensing: The Authorisation Process

- Asset-Referenced Token and E-Money Token Rules

- Crypto-Asset Whitepaper Notification Process

- Governance Requirements for MiCA Compliance

- Risk Management and Internal Controls

- Outsourcing and Cross-Border Crypto Services

- Reporting, Record-Keeping, and Ongoing Obligations

- MiCA Regulation Impact on the Crypto Industry

📌 Key Takeaways

- MiCA creates uniform EU crypto rules — replacing the patchwork of national regulations with a single framework for all 27 member states

- CASP licensing requires comprehensive compliance — including fit-and-proper assessments, capital requirements, governance structures, and business continuity plans

- Asset-referenced tokens face strict oversight — issuers must obtain separate authorization, maintain reserves, and comply with enhanced capital requirements under Article 35

- Governance standards mirror traditional finance — dual-control management, independent compliance officers, risk management functions, and internal audit are mandatory

- MFSA Rulebook evolves with EU technical standards — now on its third version (March 2026), incorporating ESMA and EBA Level 2 and Level 3 requirements

What Is MiCA Regulation and Why It Matters

The Markets in Crypto-Assets Regulation, commonly known as MiCA regulation, represents the European Union’s most ambitious attempt to create a comprehensive legal framework for the crypto industry. Established by Regulation (EU) 2023/1114, MiCA provides uniform rules across all EU member states for the issuance, trading, and servicing of crypto assets — ending years of regulatory fragmentation that created uncertainty for businesses and consumers alike.

The MFSA MiCA Rulebook, published by the Malta Financial Services Authority, translates this EU regulation into practical, enforceable rules for entities operating under Maltese jurisdiction. First issued in March 2025 and now in its third revision (March 2026), the Rulebook provides detailed guidance on authorization procedures, ongoing compliance requirements, governance standards, and reporting obligations that crypto-asset service providers (CASPs) and asset-referenced token issuers must follow.

For anyone involved in the crypto industry — whether as a service provider, token issuer, investor, or compliance professional — understanding MiCA regulation is no longer optional. It is the regulatory reality that determines market access across the world’s largest single market. This guide breaks down the MFSA MiCA Rulebook into actionable sections, explaining what each requirement means in practice and how it affects your crypto business or investment decisions.

Scope and Application of the MiCA Rulebook

The MiCA Rulebook applies to two primary categories of regulated entities: crypto-asset service providers (CASPs) and issuers of asset-referenced tokens. The rules are issued pursuant to Article 38 of Malta’s Markets in Crypto-Assets Act (Cap. 647) and are modeled on the requirements of the MiCA Regulation itself.

Critically, the Rulebook must be read in conjunction with three layers of regulation: the MiCA Regulation itself, the implementing and regulatory technical standards issued by the European Supervisory Authorities (ESMA and EBA), and Malta’s domestic MiCA Act. This multi-layered structure means that compliance requires understanding not just one document but an entire ecosystem of interconnected rules — a challenge that even experienced compliance teams find daunting.

The classification of what constitutes a crypto-asset under MiCA follows guidelines from the Joint European Supervisory Authorities, including standardized tests for determining whether a digital asset falls within scope. ESMA has also issued specific guidelines on when crypto-assets qualify as financial instruments, which determines whether MiCA or existing securities regulations apply. For context on how digital asset regulation intersects with broader financial frameworks, see our analysis of the DORA Regulation for Finance.

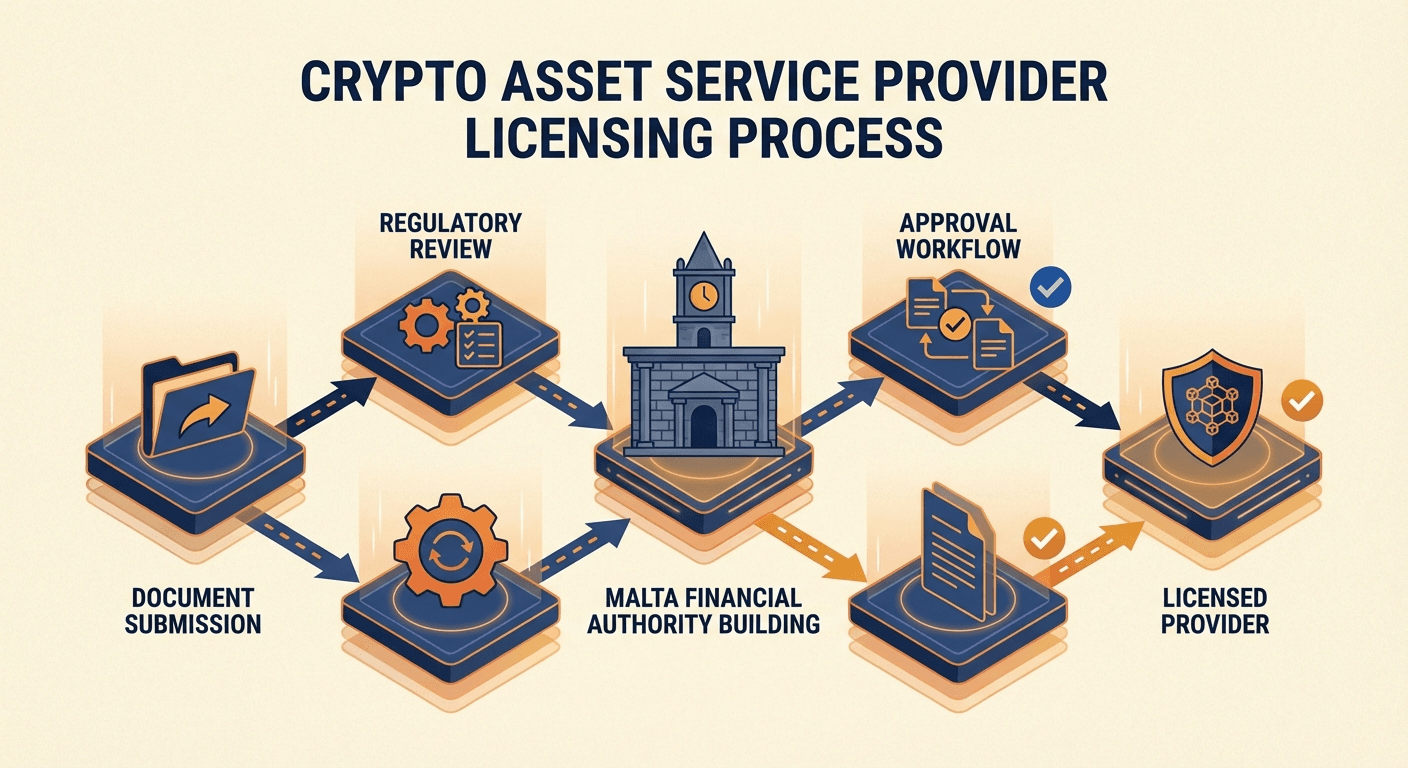

CASP Licensing: The MiCA Regulation Authorisation Process

Obtaining a Crypto-Asset Service Provider license under MiCA regulation is a rigorous, multi-stage process designed to ensure that only properly capitalized, well-governed entities can operate in the EU crypto market. The MFSA Rulebook details every step from initial application through to commencement of business.

The process begins with the submission of comprehensive application documentation, encompassing business plans, governance structures, capital adequacy demonstrations, and detailed information about all key personnel. Applicants must comply with the regulatory technical standards issued pursuant to Article 62 of the MiCA Regulation, which specify exactly what information must be provided.

A cornerstone of the licensing process is the fit-and-proper assessment, which applies to every qualifying shareholder, beneficial owner, board member, senior manager, MLRO, and compliance officer. The MFSA follows its own Guidance on Fitness and Properness Assessments alongside the Joint EBA/ESMA Guidelines on suitability assessment. The burden of proof rests with the applicant — you must affirmatively demonstrate fitness, not merely avoid disqualifying factors.

Capital requirements are non-negotiable. CASPs must demonstrate compliance with Article 67 of the MiCA Regulation, while asset-referenced token issuers must meet Article 35 requirements. These initial capital requirements must be maintained on an ongoing basis, with regular reporting to confirm continued compliance.

Transform complex regulatory documents into interactive experiences your compliance team will actually use.

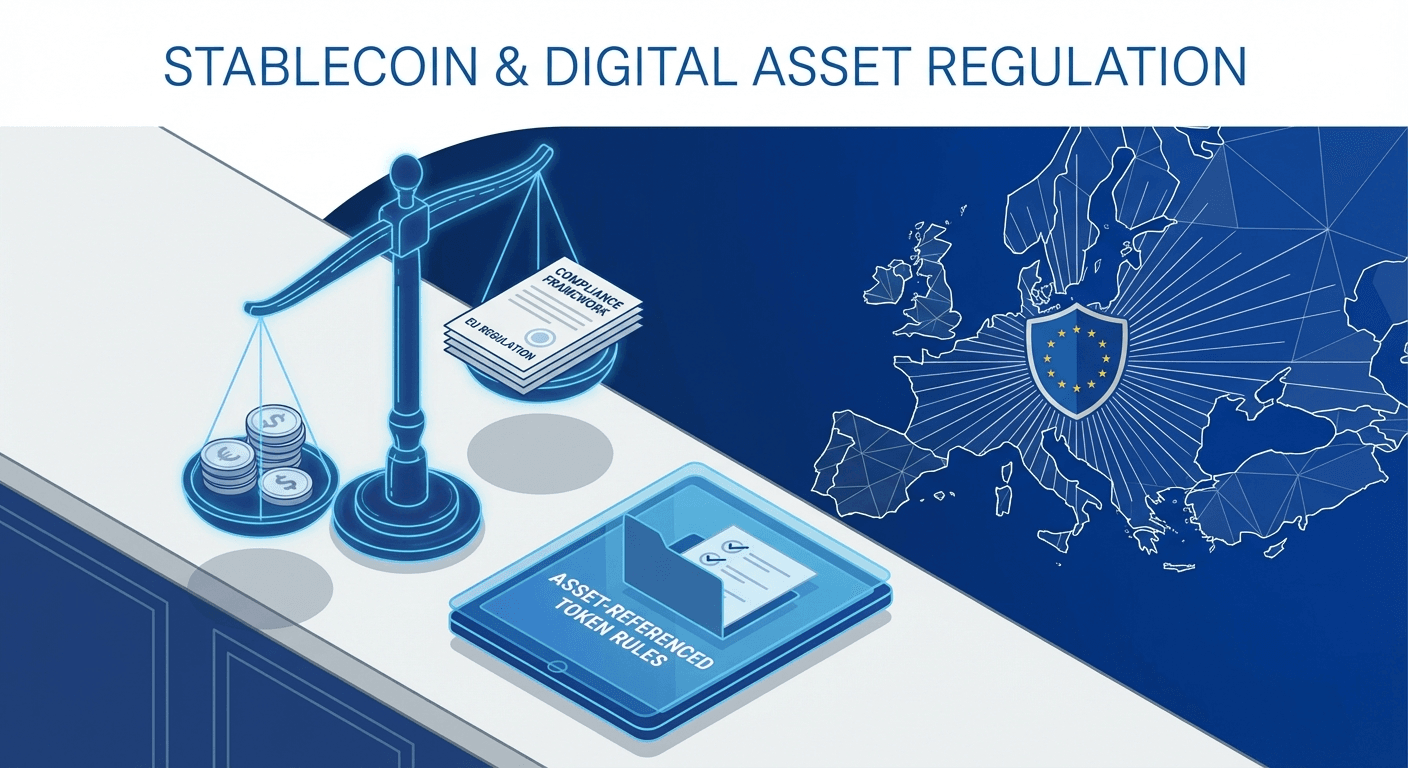

Asset-Referenced Token and E-Money Token Rules

MiCA regulation creates distinct categories for different types of stablecoins and tokens. Asset-referenced tokens (ARTs) — those maintaining value by referencing multiple currencies, commodities, or other crypto assets — face the most stringent requirements. Issuers must obtain specific authorization from the MFSA, with the whitepaper notification forming part of the application process itself.

E-money tokens (EMTs), which reference a single official currency, fall under a separate regime. Only entities already authorized as electronic money issuers or credit institutions under Malta’s Financial Institutions Act or Banking Act can issue EMTs. While the whitepaper notification process is somewhat lighter, EMT issuers must comply with both MiCA requirements and existing electronic money regulations — a dual-compliance burden that requires careful navigation.

Both ART and EMT issuers must produce detailed whitepapers that comply with specific Commission Delegated Regulations. These whitepapers must be machine-readable, include sustainability disclosures regarding the environmental impact of consensus mechanisms, and follow standardized templates. The ESMA guidelines on whitepaper content, classification methodology, and presentation are mandatory references for any issuer.

Importantly, while the MFSA does not require prior approval of whitepapers or marketing communications before publication, issuers remain fully responsible for compliance with MiCA Regulation requirements. The regulatory approach is “notify and comply” rather than “approve and operate” — meaning regulators can take enforcement action after publication if whitepapers are found to be non-compliant.

Crypto-Asset Whitepaper Notification Process

The notification process for crypto-asset whitepapers varies depending on the type of asset. For crypto-assets other than ARTs and EMTs — the broadest category including utility tokens and most cryptocurrency projects — any legal person established in Malta can submit a notification. The process requires submitting the notification form through the MFSA’s Licence Holder Portal along with applicable fees.

A notable provision in the Rulebook addresses the “limited network exclusion” under Article 4(3)(d) of the MiCA Regulation. Entities that believe their crypto-assets qualify for this exemption must still submit a Limited Network Exclusion Form to the MFSA. This ensures regulatory awareness even for assets that may ultimately fall outside MiCA’s scope, reflecting the Authority’s risk-based supervision approach.

Modified whitepapers also require notification. When any changes are made to a previously notified whitepaper, the updated version must be submitted through the LH Portal with clear indication of the changes. This ongoing notification requirement ensures that investors and the regulator always have access to current, accurate information — a key consumer protection mechanism within the MiCA framework.

MiCA Regulation Governance Requirements for Crypto Companies

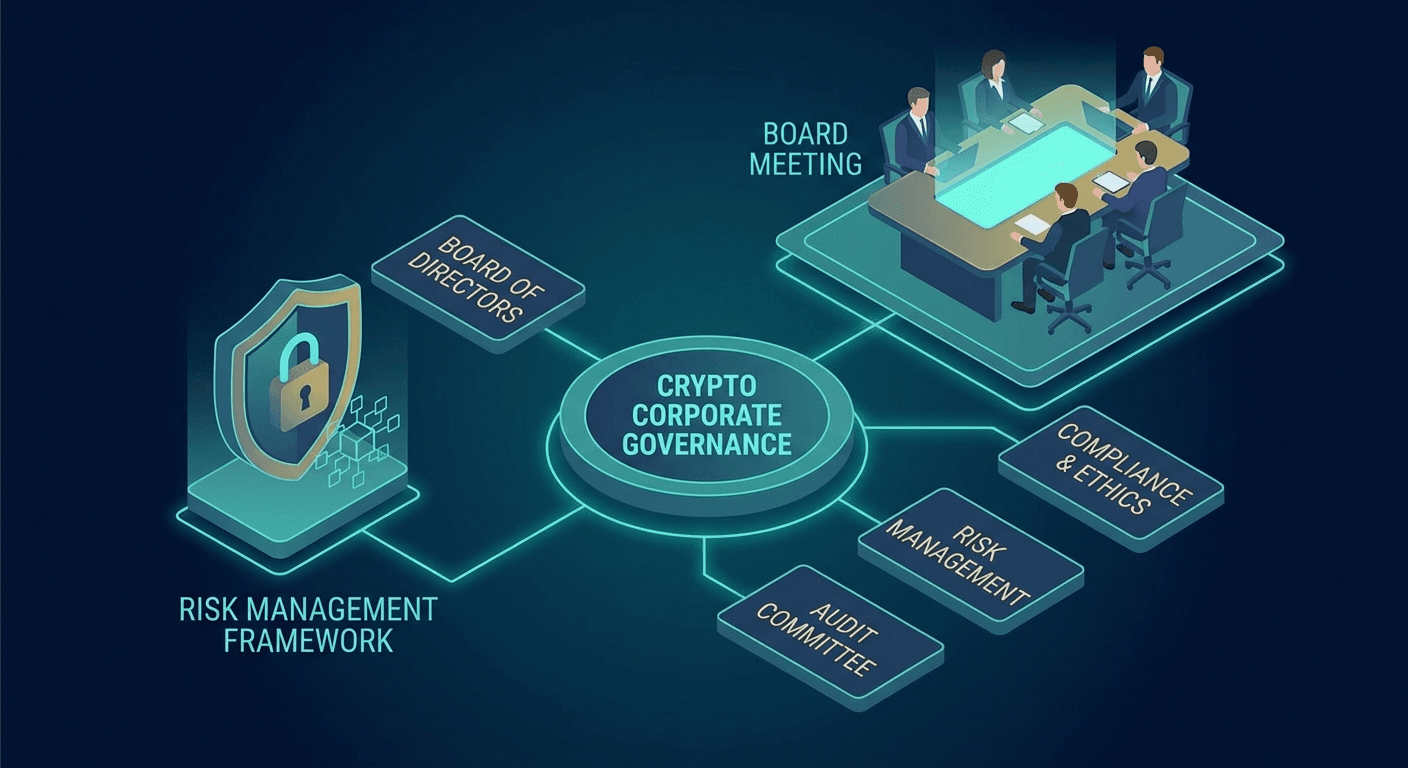

Perhaps the most transformative aspect of MiCA regulation for the crypto industry is its governance requirements, which essentially bring crypto companies in line with traditional financial services standards. The MFSA Rulebook mandates a comprehensive governance framework that would be familiar to anyone working in banking or investment services.

The dual-control principle requires that every licensed entity be effectively directed by at least two individuals of sufficiently good repute, knowledge, and experience. At least one executive director must be based in Malta, ensuring local substance and accountability. The Board of Directors bears overall responsibility for compliance, strategic oversight, risk management, remuneration policies, and the integrity of financial reporting systems.

The compliance function must operate independently, with a dedicated Compliance Officer approved by the MFSA. This officer cannot be involved in the operations they oversee — creating a clear separation between business activities and regulatory monitoring. The Compliance Officer must maintain a monitoring plan, submit periodic reports to the Board, and ensure that all regulatory breaches are documented and addressed. The role carries personal responsibility: evidence of bad faith, incompetence, or deceptive behavior is treated as a serious regulatory matter.

Similarly, every licensed entity must appoint a Money Laundering Reporting Officer (MLRO) who understands the full extent of AML/CFT obligations. The MLRO role can be combined with the Compliance Officer role, but both carry significant personal liability and the MFSA expects individuals to fully understand their responsibilities before accepting appointment. For related regulatory frameworks, our guide on the NIST Cybersecurity Framework provides complementary security perspectives.

Make regulatory compliance engaging — turn dense rulebooks into interactive learning experiences for your team.

Risk Management and Internal Controls Under MiCA

MiCA regulation requires crypto companies to establish risk management frameworks comparable to those in traditional banking. The Rulebook mandates that licensed entities maintain risk management policies identifying all risks related to their activities, set appropriate risk tolerance levels, and adopt effective arrangements to manage those risks.

The risk management function must operate independently, implementing policies, providing reports to senior management, developing risk strategy, and maintaining direct communication with the Board — bypassing senior management when necessary. This last provision is crucial: it ensures that risk concerns cannot be suppressed by operational leadership before reaching the Board.

A comprehensive risk management framework assessment must be conducted at least annually, evaluating the effectiveness of key processes, controls, and procedures. The assessment must account for changes in the operational environment, regulatory requirements, and risk profile. This annual review requirement ensures that risk management evolves alongside the rapidly changing crypto landscape.

Internal audit functions must also be established, operating separately from all other functions. The internal audit team must maintain an audit plan, issue recommendations, verify compliance, and report to the Board. The MFSA may exempt smaller or simpler entities from this requirement, but the threshold for exemption is high — the entity must demonstrate that a full internal audit function would be disproportionate given its scale and complexity.

Business continuity planning under MiCA is linked to the Digital Operational Resilience Act (DORA) requirements. Licensed entities must establish ICT business continuity plans, response and recovery plans, and ensure that crypto-asset services can be maintained or quickly resumed following any disruption. The integration of DORA and MiCA creates a comprehensive operational resilience framework for the crypto sector.

Outsourcing and Cross-Border MiCA Crypto Services

Outsourcing critical or important operational functions under MiCA regulation requires careful planning and regulatory notification. The MFSA must be notified at least 60 calendar days before entering into any outsourcing arrangement for critical functions. The Rulebook provides detailed criteria for determining whether a function is critical, including assessment of potential impacts on financial resilience, business continuity, operational risk, and client services.

The assessment framework for outsourcing is remarkably thorough. Entities must consider the substitutability of the arrangement, the aggregated exposure to any single service provider, the potential for scaling, data protection implications under GDPR, and the ability to reintegrate functions if necessary. The MFSA reserves the right to limit, restrict, or require the cancellation of outsourcing arrangements that compromise governance or supervisory capability.

Cross-border provision of crypto services within the EU follows the MiCA passporting regime under Article 65. Licensed entities intending to operate across member states must submit a Cross-Border Provision of Services Notification Form to the MFSA, which then communicates with the host state authorities. Any changes to cross-border arrangements must be notified immediately. This passporting mechanism is one of MiCA’s most significant benefits — a single license can provide access to the entire EU market of 450 million consumers.

Help your compliance team master complex regulations — transform PDFs into engaging interactive experiences.

Reporting, Record-Keeping, and Ongoing Obligations

The ongoing obligations under MiCA regulation are extensive and detailed. Licensed entities must notify the MFSA of a wide range of events, from fraud discoveries and hacking incidents to material legal proceedings and changes in key personnel. These notifications must be made “immediately upon becoming aware” — there is no grace period for disclosing material events.

Prior approval from the MFSA is required for more significant changes, including changes to registered names, capital structure, mergers or sales, appointment of directors or senior managers, and material changes to responsibilities. The distinction between notification requirements and prior approval requirements is a critical compliance consideration — acting without required approval can constitute a regulatory breach.

Record-keeping requirements mandate that all crypto-asset services, activities, orders, and transactions be recorded with sufficient detail for supervisory purposes. Trading platforms must maintain order book records for at least five years and provide regulators with access to this data. Pre-trade and post-trade transparency data must be made publicly available, bringing crypto trading closer to the transparency standards that govern traditional securities markets.

Audited annual returns must be submitted within six months of the accounting reference date, including financial statements prepared in accordance with the Companies Act and generally accepted accounting principles. These reporting requirements ensure that regulators maintain ongoing visibility into the financial health and operational integrity of licensed entities. For additional perspective on how financial reporting requirements are evolving, see our analysis of the ECB Annual Report 2024.

MiCA Regulation Impact on the Crypto Industry

The MiCA regulation represents a paradigm shift for the European crypto industry. By establishing clear, harmonized rules across 27 member states, it eliminates the regulatory arbitrage that previously characterized the EU crypto landscape. Companies can no longer forum-shop for the most lenient jurisdiction — instead, they must meet a uniform baseline of compliance that brings the sector closer to traditional financial services standards.

For established crypto businesses, MiCA creates both challenges and opportunities. The compliance costs are significant — governance structures, personnel requirements, capital adequacy, and ongoing reporting create substantial overhead. However, the regulatory clarity reduces legal uncertainty and creates a defensible market position against unregulated competitors. The passporting mechanism, allowing a single license to access the entire EU market, represents a major competitive advantage for compliant firms.

The environmental sustainability requirements are particularly noteworthy. By mandating disclosure of consensus mechanism impacts on climate and the environment, MiCA pushes the crypto industry toward greater transparency about its environmental footprint. This aligns with the EU’s broader sustainability agenda and may accelerate the shift toward more energy-efficient blockchain protocols across the market.

Looking ahead, the MiCA framework will continue to evolve as ESMA and EBA issue additional technical standards and guidelines. The MFSA Rulebook’s three revisions in its first year demonstrate the regulatory framework’s dynamic nature. For crypto businesses operating or planning to operate in the EU, ongoing monitoring of regulatory developments is essential. The a16z State of Crypto 2024 report provides useful market context for understanding how regulation shapes investment flows in this sector.

Frequently Asked Questions

What is MiCA regulation for crypto assets?

MiCA (Markets in Crypto-Assets) is the EU’s comprehensive regulatory framework for crypto assets, established by Regulation (EU) 2023/1114. It creates uniform rules across all EU member states for crypto asset issuance, trading, and service provision, covering transparency, disclosure, authorization, and supervision requirements for crypto-asset service providers (CASPs) and token issuers.

How do you get a CASP license under MiCA?

To obtain a CASP (Crypto-Asset Service Provider) license under MiCA, applicants must submit a comprehensive application to their national competent authority (such as MFSA in Malta), demonstrate compliance with capital requirements under Article 67, pass fit-and-proper assessments for all key personnel, establish governance frameworks including compliance and risk management functions, and fulfill pre-licensing conditions within six months of in-principle approval.

What are asset-referenced tokens under MiCA?

Asset-referenced tokens (ARTs) are crypto assets that maintain a stable value by referencing multiple currencies, commodities, or other crypto assets. Under MiCA, ART issuers must obtain specific authorization, comply with Article 35 capital requirements, submit detailed whitepapers, maintain reserves, and meet ongoing governance and reporting obligations set by their national competent authority.

What compliance requirements does MiCA impose on crypto companies?

MiCA requires crypto companies to maintain robust governance with dual-control management, appoint compliance officers and MLROs, implement risk management frameworks, establish business continuity plans compliant with DORA (EU 2022/2554), maintain detailed record-keeping for at least five years, handle customer complaints transparently, manage conflicts of interest, and submit audited annual returns to their regulator.

When did MiCA regulation come into effect?

MiCA Regulation (EU) 2023/1114 was adopted in May 2023 with phased implementation. The MFSA published its initial MiCA Rulebook in March 2025, with subsequent updates in June 2025 and March 2026 incorporating new Level 2 and Level 3 requirements from ESMA and EBA technical standards.